Macro is the Weather. Part 3.

Macro is the Weather. Part 3.

Give them VIX. Lots of VIX!

In Parts 1 & 2 we saw how and why the markets react (and most often vastly over-react) to events due to marginal changes in liquidity. I have also argued that all the reasons behind the over-reaction function are in trend and unlikely to get better without some changes in regulation or action from Central Banks (CBs). In this concluding Part 3, I want to examine the part played currently in the markets by CBs and how and why I would amend and extend their current policies to better achieve market goals.

CBs attempt to influence the asset markets through two main mechanisms, both executed via the Open Market Operations (OMOs) they conduct.

The first is the traditional and familiar setting of Fed Fund rates. By influencing overnight rates, they can influence the whole of the shorter end of the yield curve, with those effects rippling along via purely market mechanisms to the longer end of the Treasury curve. Nothing controversial here. But during times of high stress, they found that it was not really the level of short rates that was a problem but rather the shape of the curve, the spread to corporates and the transmission mechanism to other asset classes that broke down. Imagine if you will that you are a bank. A very bad recession is coming and your clients need financing to bridge that recession. They probably need funding for 4-5 years (or longer) to weather a recession which might last only a year and another 2-3-4 years for their balance sheet to recover sufficiently for them to be in a position to repay your loan. Your primary concern here is not the interest rate you will charge, but rather your judgement as to how impaired their balance sheet might become (IE: will they ever be in a position to repay?). If your judgement is that they are unlikely to be able to repay because of the severity of the recession, their current leverage or any other reason, you won’t lend, regardless of the interest rate. You will deem it safer to just sit on liquidity even though it is lowering your ROA. At least you will have an ROA! Any OMOs carried out by the CB to lower Fed Funds rates will only lower the yield of short term Treasuries and do nothing for the spread between Treasuries and Corporate Bonds, which might even continue ballooning out further. End result: nothing much has changed: the corporate sector gets no funding. Only difference will be the level at which the Government funds its deficit and the level at which banks lend their excess liquidity to each other at the very short end. Main Street is still screwed. As the spread of USTs to corporates continue to balloon, equities get sold and the wealth effect goes into reverse.

Which brings us to the second mechanism: Quantitative Easing (QE). This was really pioneered by the Bank of Japan starting in the early 2000s and imitated by the US (and the ECB much later) during and after the Great Financial Crisis which started in 2008. QE is often misunderstood and its effects completely misrepresented. It is NOT money printing. It is simply the purchase of bonds (mortgages, treasuries, corporates) in exchange for their current market value in cash, from and to the banks that are members of the CB’s system. It is designed to lower the yield curve (not necessarily to flatten it, that is worthy of a completely separate piece) and also to maintain or tighten the spread to corporates and mortgage backed securities. To understand why this “works”, you have to understand the relationship between corporate bonds and equities. And to an even greater extent: mass psychology. As the CB lowers the Treasury curve and simultaneously stabilizes or shrinks the spread to corporate and other bonds, it encourages risk-taking by forcing equity valuations higher via the narrowing of corporate spreads. And shifts the marginal liquidity balance between Risk On and Risk Off. It’s really a confidence building measure.

You know that you have a huge player with bottomless pockets on your side. If you are a bank you can shift as much current corporate debt (that you are worried about defaulting) from you balance sheet to the CB’s, completely transferring that default risk. In exchange for cash. With the cash you can make new loans or purchase other risk assets, which lowers spreads further. And so on, in a virtuous circle. The CB has now taken the risk on its balance sheet and will sit on it until it matures, freeing up bank capital at market levels for a new cycle of lending, at lowered market rates.

In complete layman terms: imagine if a helicopter dropped money from the sky. You pick it up and put it in your pocket. You might still get fired tomorrow but you feel a lot better about your prospects knowing you have some money in your pocket regardless. Your confidence has been boosted.

It cannot be argued that QE does not work. But it can be argued that it has some very unpleasant side effects, which might in the long term outweigh its benefits.

One side effect is that it makes the markets dependent on it. It’s addictive. Banks now know that they have a safety net for their lending spreads and will lower their standards in a chase for corporate yield at sub-market levels. And it encourages speculative moves in lower quality assets by driving their value away from market fair value. The other side effect is that it is irreversible, if you want to maintain the current relative value of assets. You cannot stop it or drive it in reverse if you don’t want a politically unacceptable swing back in relative values between bonds and equities and the funding level of government deficits. And all CBs might maintain that they are independent and apolitical but…they simply are not. That is the reality, unfortunately.

Don’t get me wrong, QE had its place in 2008. It was the right thing to do. It mitigated an episode of huge wealth destruction and stopped it spreading to every area of the economy, healthy or not, guilty or innocent of its causes. But it should have been scaled back and finally stopped by 2017, when every part of the economy had quite clearly fully recovered. That it was not, is proof positive of the political impossibility of its termination in countries with short political cycles. It can only be done at the very beginning of an Administration that is willing to sit with the pain for the first 2-3 years in exchange for the longer term gain. Don’t hold your breath. Janet Yellen sure didn’t…and now she is Secretary of the Treasury and a few $m richer.

But the 2020 Covid19 crisis was not an episode of wealth destruction, unlike 2008. The economy was doing great before it and would continue to do great once the virus was eradicated. It did not, in my opinion, call for QE. It called for 2 things:

1. A full time bridge between the onset of the pandemic and its end (however achieved: natural burn-out, vaccine, etc.). The needed response was legislative and entirely fiscal: rent freezes, loan deferments, with corresponding guarantees for the lenders and personal income guarantees for workers, for the entire duration. This would have insulated the entire economy from any long term damage.

2. A reduction or cap in short term Volatility.

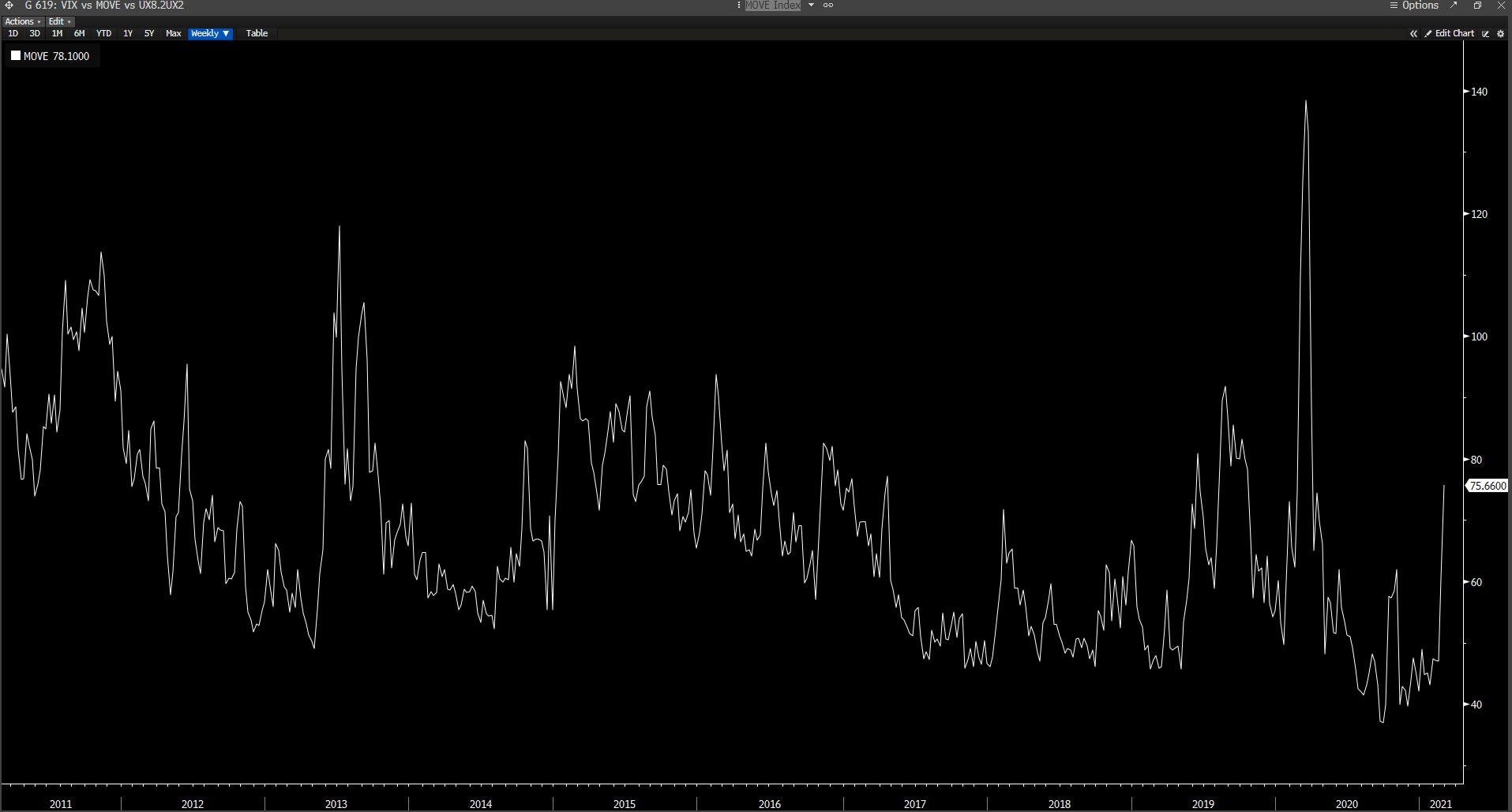

It is this second point that I would use in such a situation if I were running a Central Bank. To understand the importance of volatility to the current interplay between assets you have to appreciate the interplay between Risk On and Risk Off. I have found no better place to follow that key relationship than www.riskdials.com. During periods of Risk Off, investors sell risky equities and buy riskless government bonds. And what did the Fed do during a period of obvious Risk Off? It poured petrol on the fire by stepping in and buying MORE bonds via QE, when the entire world was buying bonds!!? What did this achieve? An even sharper increase in the MOVE Index, the implied volatility of bond options, as can be seen in this chart. Look at the spike in early 2020:

There is no doubt about the interplay between the MOVE index and VIX, the volatility index of equities. They are two sides of the same coin and they spike and ebb together:

By activating QE, the Fed actually made the situation in the equity markets worse, not better, in the very short term. A market in which every risk strategy was being blown up by everything I described in Part 2 (reminder: irrational fear, media hysteria, high starting leverage, automatic stops driven by technology and the illiquidity caused by Dodd-Frank) needed time to adjust and a supply of volatility. As gammas and vannas cascaded and rampaged through every portfolio and structured product, causing them to be automatically stopped at market, when bid-offer spreads had already ballooned out of sight, the Fed actually helped spike the VIX. Great thinking!

Had the Fed actually offered to sell unlimited quantities of VIX futures at, say, 40%, what would have happened?

1. Bid-offer spreads would immediately have tightened.

2. Gamma changes would have stabilized. Deltas would have been reduced quicker.

3. Leverage could have been reduced much more efficiently.

And it would have given people time to start thinking like this:

“OK, we will have at most 2 years of reduced earnings at worst, while we fight this pandemic, then we will return to $150-160 forward earnings quite quickly. What discount rate do I wish to apply to those 2 years (even if earnings are almost zero) and how quickly will we be back to $150-160 forward earnings in 2022 and what multiple do I apply to those earnings? It was x20 before this pandemic. But now bond yields are much lower so maybe slightly higher? x21/x22?”

By my calculations we would have stopped at 2800 SPX at worst. And all without QE and the hangover we are currently suffering in the bond markets as a consequence.

The Fed would have lowered volatility, given the markets a softer landing, made a ton of money when those VIX futures contract expired and not bought a single Treasury. They maybe would have needed to buy junk bonds. Maybe. I will concede that.

Something for the CBs to think about introducing into their armory. A step to a market solution because not every smaller crisis calls for the same tools as solutions as the 2008 Great Financial Crisis did. Start thinking out of your comfort zone, CBs!

"FED poured petrol on the fire by stepping in and buying MORE bonds via QE, when the entire world was buying bonds". Didn't the FED step in to buy government & corporate bonds as the entire world was selling those bonds and move into cash? FED didn't add petrol on the fire. They prevented the collapse of the fixed income market by capping what was supposed to be the risk-free curve.

Very interesting article, thanks for writing this!